A lienholder title is a vehicle ownership record that shows a lender or financing company has a legal financial interest in the vehicle. Because most vehicles are purchased with loans, lienholder titles are extremely common. Therefore, understanding how lienholder titles work helps owners avoid transfer delays, protects buyers from hidden debt claims, and ensures the vehicle can be legally sold once the loan is paid.

How a Lienholder Is Recorded on a Vehicle Title

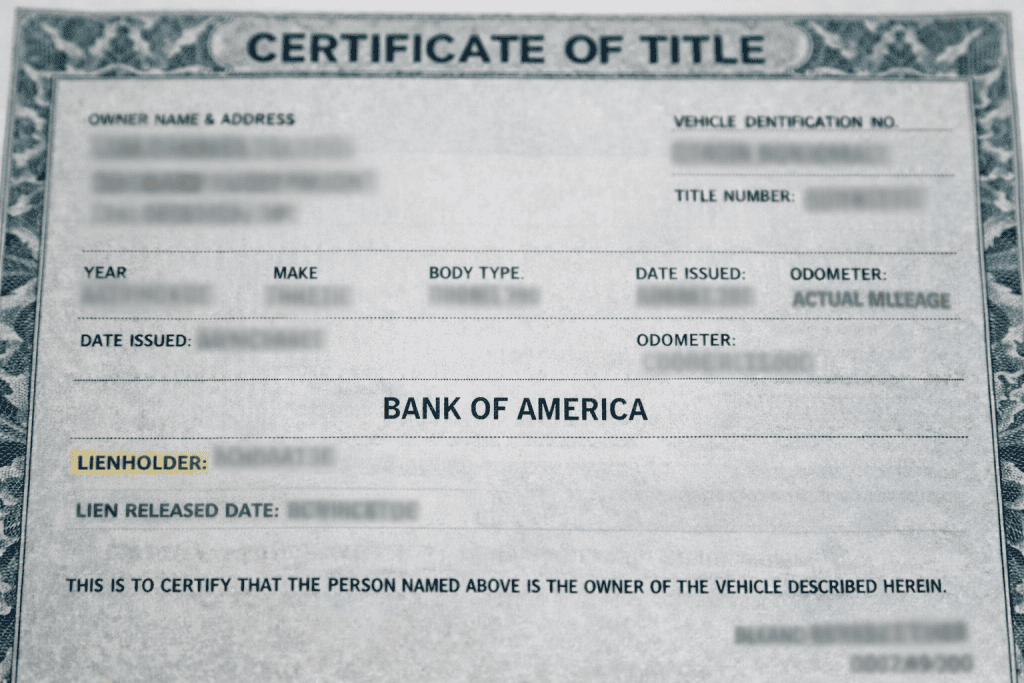

Example vehicle title showing lienholder information highlighted on official ownership document.

When a vehicle is financed, the lender files a lien with the state motor vehicle agency. As a result, the title record lists the lender as the lienholder while the buyer is recorded as the registered owner.

This arrangement gives the lender legal protection. If loan payments stop, the lien allows the lender to reclaim the vehicle through repossession procedures. Meanwhile, the borrower keeps possession and normal use of the vehicle as long as payments remain current.

Depending on the state, either the owner or the lender may hold the physical title document. However, the electronic state record always reflects the lien until it is officially released.

How Lienholder Titles Affect Ownership Rights

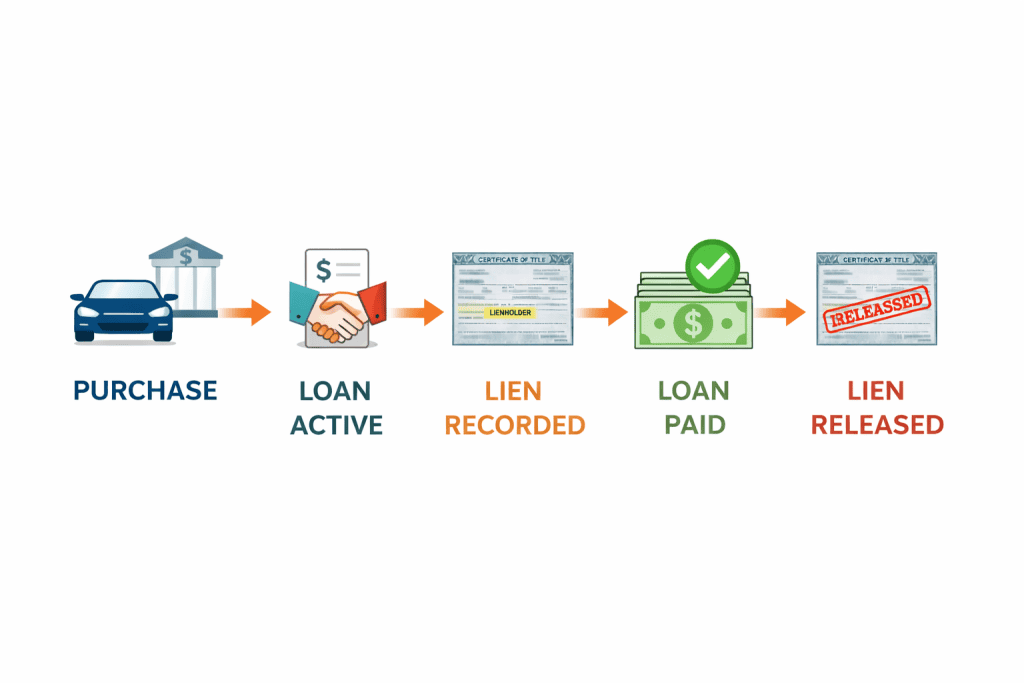

Diagram showing how a car loan leads to a lien on the title and how payoff results in lien release and a clear title.

Although the buyer drives the vehicle, the lien restricts full ownership control. For example, the owner typically cannot legally sell, transfer, or re-title the vehicle without satisfying the loan balance first. Therefore, the lienholder must approve the payoff and release the lien before ownership transfer can proceed.

Additionally, many lenders require borrowers to maintain specific insurance coverage levels while the lien is active. This requirement protects the lender’s financial interest if the vehicle is damaged or totaled.

Because these restrictions are tied to the loan agreement, they remain in force until the debt is cleared.

How Lien Releases Work After Loan Payoff

Once the loan balance is fully paid, the lender issues an official lien release. This release may be sent electronically to the state motor vehicle agency or provided as a paper document to the owner.

Afterward, the owner can request a new title showing no active lien. In electronic-title states, this update may occur automatically. However, in paper-title states, the owner may need to submit the lien release to receive an updated certificate.

Because processing timelines vary, confirming the lien removal before attempting to sell the vehicle prevents unexpected delays.

How Buying a Vehicle With an Existing Lien Works

Purchasing a vehicle that still has an active lien requires additional steps. First, the seller must obtain an official payoff amount from the lender. Then, the buyer typically pays the lender directly or completes the transaction through a dealership or escrow service to ensure the lien is cleared.

Only after the lender confirms payment can the title transfer proceed.

Because improper handling of lien payoffs can leave the buyer without legal ownership, verifying that the lien release has been officially recorded is essential before completing the purchase.

How State Electronic Title Systems Change the Process

Many states now use electronic lien and title systems rather than physical certificates. In these systems, the lienholder often holds the digital title record until the loan is paid.

As a result, the owner may never receive a paper title until the lien is released. While this simplifies recordkeeping, it also means buyers must confirm title status through official state systems rather than relying solely on physical documents.

Therefore, checking the state motor vehicle database or obtaining lender confirmation is often the most reliable verification method.

How Lienholder Titles Affect Resale Value and Transactions

A lien does not automatically reduce vehicle value, because it reflects financing status rather than damage history. However, it can slow private sales if payoff documentation is incomplete.

Additionally, buyers often prefer vehicles with no liens because the ownership transfer process is simpler. Consequently, sellers planning to list their vehicle privately often clear the lien first to streamline the transaction and reduce buyer hesitation.

Why Understanding Lienholder Titles Protects Buyers and Owners

Understanding how lienholder titles function ensures that ownership transfers occur legally and without financial disputes. While liens are normal in financed purchases, failing to confirm lien release can delay registration, block resale, or create legal ownership conflicts.

Therefore, verifying lien status should always be part of both buying and selling procedures. When the process is handled correctly, lienholder titles present no long-term ownership risk once the debt is satisfied and officially removed.

This platform analyzes depreciation trends, resale value behavior, and long-term ownership costs, helping drivers understand how mileage, maintenance, and timing shape real financial outcomes.